It doesn’t matter how one feels* about AI as a technological problem. It is much more of a financial problem, a threat similar to others that preceded it but special in its own special way. Purveyors already know the limits of the technology but dangle the potential profits as unlimited.

Because all the convenient confusion can be difficult to parse, a cultural interpretation of the crisis requires urgent attention. And thanks to Short Attention Span Theater – the single, unwavering truism threading society together – it needs to be brief and concise. Enter The Great Crash, 1929 by John Kenneth Galbraith into evidence:

…there is deep faith in the power of incantation. When the market fell many Wall Street citizens immediately sensed the real danger, which was that income and employment – prosperity in general – would be adversely affected. This had to be prevented. Preventive incantation required that as many important people as possible repeat as firmly as they could that it wouldn’t happen. This they did. They explained how the stock market was merely the froth and that the real substance of economic life rested in production , employment, and spending, all of which would remain unaffected. No one knew for sure this was so. As an instrument of economic policy, incantation does not permit of minor doubts or scruples.

To the mighty extent that AI hype runs riot, our savvy age turns the power of incantation into cynicism verging on a new art form. Machine learning is so deeply ingrained into every sector that it simply must work and cannot fail, to coin a phrase. It must be powerful if important people are warning that it might take over.

Meanwhile, circularity: Tech giants investing in each other’s AI products and projects, driving valuation and demand for power, water, chips, and data centers, and inflating the perception of market consensus. We love the miasma of mortgage-backed securities in the morning.

Circularity > singularity.

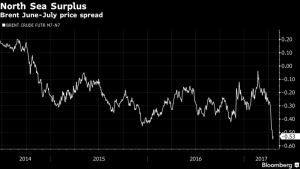

Image: Screenshot from Bloomberg March 20, 2026

In early September 2008, I drove down to Charleston to visit a cousin who had recently suffered a terrible accident. Throughout the drive I listened to extended public radio reports on an evolving calamity: the collapse of Lehman Brothers financial services firm. The horror that the government was going to allow such a large firm to go under was decorated with the baroque gadgetry of terms that would become more familiar in the coming years: credit default swaps, subprime mortgage lending, tranches, CDOs. The gore and detail of the cover that had been constructed around scams and fraud at the broadest level was audible in the voices of interviewers and guests. There was a tinge of disbelief within their attempts to explain what these terms meant and how they had gotten us all (!) into so much peril. It was as close to 1929 as we had come and potentially far worse – so extensively had the giant vampire squid of financial engineering welded its tentacles to every sector. Housing, banking, investing, construction, debt, bonds… this is business America now, and every other activity is vulnerable to its caprice. It was the stretch run of a presidential election as well; one candidate tried to suspend the campaign, the other fortunately tried to hold things together.

In early September 2008, I drove down to Charleston to visit a cousin who had recently suffered a terrible accident. Throughout the drive I listened to extended public radio reports on an evolving calamity: the collapse of Lehman Brothers financial services firm. The horror that the government was going to allow such a large firm to go under was decorated with the baroque gadgetry of terms that would become more familiar in the coming years: credit default swaps, subprime mortgage lending, tranches, CDOs. The gore and detail of the cover that had been constructed around scams and fraud at the broadest level was audible in the voices of interviewers and guests. There was a tinge of disbelief within their attempts to explain what these terms meant and how they had gotten us all (!) into so much peril. It was as close to 1929 as we had come and potentially far worse – so extensively had the giant vampire squid of financial engineering welded its tentacles to every sector. Housing, banking, investing, construction, debt, bonds… this is business America now, and every other activity is vulnerable to its caprice. It was the stretch run of a presidential election as well; one candidate tried to suspend the campaign, the other fortunately tried to hold things together. We wish they were more rare. But just as rising wages are bad news for business(?) and solar most horribly spells doom for coal, word in the oil game is that consistent catastrophes are needed

We wish they were more rare. But just as rising wages are bad news for business(?) and solar most horribly spells doom for coal, word in the oil game is that consistent catastrophes are needed